Features / Focus

What’s Next?

The Future of the Asian Art Market (1)

1. The Asian Art Market ; Clare McAndrew

2. The Diverse Identity of the Asian Art Market ; Adeline Ooi

posted 17 Sep 2018

Panelist Clare McAndrew

This conversation aims at providing an overview of the present and future of Asian art in the global art market, addressing the question ‘Is Asian content competitive enough in the global art market?’ Melanie Gerlis, columnist of the [Financial Times], Clare McAndrew, author of the “Art Basel and UBS Global Art Market Report 2017”, Adeline Ooi, Asian director of 《Art Basel》, Filipa Ramos, editor-in-chief of [Art Agenda], and Amy Sherlock, deputy editor of [Frieze] magazine join the discussion.

Panelists

Clare McAndrew

Adeline Ooi

Filipa Ramos

Amy Sherlock

Moderator

Melanie Gerlis

Organizer

![]()

Speakers’ Profile

|

Clare McAndrew / Panelist Dr. Clare McAndrew is a cultural economist, investment analyst and author. McAndrew founded [Arts Economics] in 2005. [Arts Economics] is an economic research firm focused exclusively on the fine and decorative art market. McAndrew has been presenting annual reports on the global art market, and has conducted several research projects dealing with the impact of regulation and taxation on the market. She has authored the “TEFAF Art Market Report” from 2008 to 2015 and has recently been commissioned by 《Art Basel》 to further research the art market. |

|

Adeline Ooi / Panelist Adeline Ooi served for two years as an 《Art Basel》’s VIP relations manager for Southeast Asia, covering Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam from 2011 to 2013. In 2009, she co-founded a cultural agency based in Malaysia, where her clients included artists, galleries, institutions, and both corporate and private collectors. From 2006 to 2008, she worked as a curator and a program director of Valentine Willie Fine Art gallery in Kuala Lumpur. |

|

Filipa Ramos / Panelist Filipa Ramos is the editorin-chief of [Art Agenda], a world-renowned art media platform. She has lectured at Kingston University in London and Central Saint Martins. Ramos is the co-curator of Vdrome, a platform that presents works that cross the genre of modern art and cinema. She was also a research curator for 《Kassel Documenta》 in 2012 and 2017. Ramos is the co-writer of 『Lost and Found: Crisis of Memory in Contemporary Art』. |

|

Amy Sherlock / Panelist Amy Sherlock is the editorin-chief of [Frieze] magazine, a magazine leading in the discourse of contemporary art. She also has a wealth of experience covering the Asian art scene. Sherlock has worked simultaneously as a freelance exhibition organizer and a director of 《Open Source London》, London’s contemporary art festival in 2016. |

|

Melanie Gerlis / Moderator Melanie Gerlis is an art market columnist and contributor for the [Financial Times]. She was previously the art market editor for [The Art Newspaper], reporting on auctions, art fairs and market news globally since 2007. Before entering the art world, Gerlis worked for 10 years at Finsbury, a strategic communications and investor relations firm, advising investment banks, hedge funds and other financial services clients. |

Panel Talk

Melanie Gerlis: Thank you for coming to the last session today: ‘What’s Next? The Future of the Asian Art Market?’, which is a great question. I have some fantastic panelists to help answer that. I am just going to say a few words by way of introduction to just give a bit of context.

I have worked as a journalist in the art market for 11 years. I started at [The Art Newspaper], which is a newspaper that covers all aspects of art. It’s not just the art market—museums, policy, regulation, anything that touches the cultural world. It’s quite rare in that world that the art market makes front-page news, but I remember two times in particular when it did. The first was in 2011 when a report written by the brilliant Clare McAndrew on my far left here, found in 2010 that China had overtaken the UK art market and become the second biggest art market in the world by value of sales. It was only by 1%, I think, but it was quite dramatic change. Suddenly, we had to learn about auction houses such as China Guardian and Poly Auction, we went to art fairs such as 《ARTHK(Hong Kong International Art Fair)》 which later became 《Art Basel Hong Kong》, which Adeline on my left now runs for 《Art Basel》 in Asia.

The second time when Asia made big news in London was when I did a bit of number crunching and found those two auction houses’ sales had halved by the next year, 2012. It seemed to a lot of us who have seen markets and buyers come and go—from Russia, the Middle East, and South America—that the China and the Asia story was another flash in the pan. There were problems. There were questions about the data in the first place. There were reports about people bidding for works but not actually buying them. It seemed quite easy to write off. One of my greatest surprises—a very, very pleasant surprise—is that it was wrong to write it off. The growth of the art market, art enthusiasts in China and the speed of that enthusiasm have been extraordinary and very real. Just yesterday, I had to write an article about Hauser & Wirth, a huge international gallery, opening in Hong Kong. Actually, they are little late to the game, this has been happening for a while, but they are now also opening offices in Shanghai and Beijing. Of course, we are just not talking about Hong Kong and China anymore. I am excited to be here now to see all of the art fairs and galleries I’ve only previously seen in booths at art fairs. To see people in action is extraordinary here. There’s a real energy. There are many other cities in Asia adding their perspectives and talents to our world, and all of this comes at a time when markets elsewhere, particularly in Europe, where I am from, are quite fragile. We need you all. I suspect the title of this session shouldn’t be ‘The Future of the Asian Art Market’ but ‘The Future Is the Asian Art Market’. I greatly look forward to hearing the views of our excellent speakers. I will give them 10 to 15 minutes each, which will give you a bit more detail about them.

We’ll start with Clare McAndrew, who is an independent cultural economist and founded [Arts Economics] in 2005. Clare’s annual number crunching of the art market, now commissioned by 《Art Basel》 and UBS, has become an art market bible, so I really look forward to hearing what she has to say.

1. The Asian Art Market ; Clare McAndrew

Clare McAndrew ⓒGallery Weekend Korea

*Draft

Growth in the Asian art market has been one of the defining trends in the art market in the last 10 years. Global sales of art and antiques have seen massive growth over the last 20 years, and a significant impetus for that has been sales in Asia, particularly in China, as well as Asian demand for art and antiques in the global markets.

The significant changes in the market’s geographical buying and selling structure have made it more globally diversified, protecting it from external downside risks. This is evident in how the market bounced back so rapidly after the recession in 2009, versus previous historical examples, such as the early 1990s, where sales were predominantly centered only in the US and Europe.

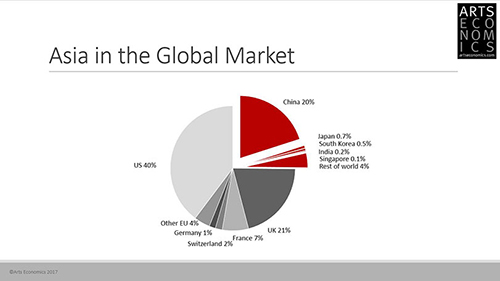

Sales of art and antiques in Asia now account for around one quarter of the global total by value, and China accounts for around 80% of that share, being by far the largest market in Asia. The ascent of China over the last 10 years has been phenomenal, with the market tripling in size, and temporarily becoming the largest market worldwide in 2011.

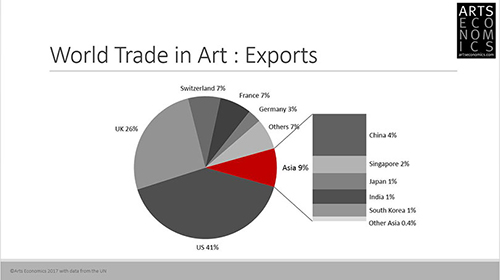

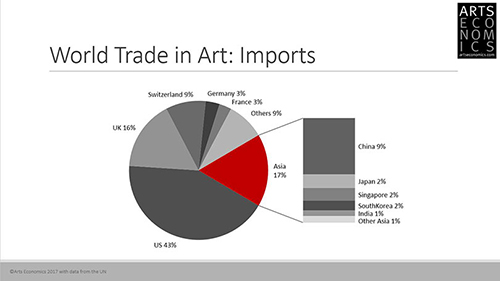

While China (and especially Hong Kong) has become an important trading hub, many other markets are more local in nature. In terms of cross-border trade, Asia’s share of exports is relatively small at 9% (with China accounting for close to half of that share). However, the region is an important importer of art, accounting for 17% of global imports of art and antiques. As wealth in Asia has grown, demand for art as luxury goods has increased. This demand has been met through local sales of art as well as purchasing abroad by Asian collectors in already established markets, such as London and New York.

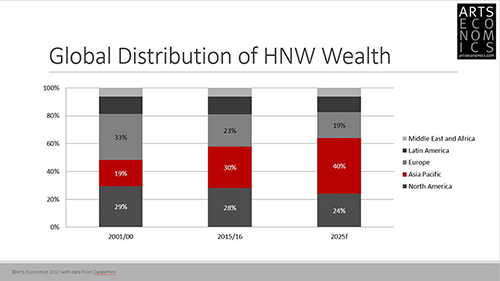

This buying power is being fuelled by shifting wealth fundamentals in the region. Average incomes in Asia are by far the fastest growing worldwide, although it is still a relatively small proportion of the population in many countries in the region that is actively engaged in the global art market. Asia has, however, also seen a very rapid increase in the number of millionaires and particularly billionaires in recent years. A recent report by UBS found that one billionaire is created in Asia every three days, outpacing all other regions in the world. Last year, high net worth (HNW) wealth in the Asia Pacific region surpassed North America, and it is excepted that by 2022 it will account for 40% of the total.

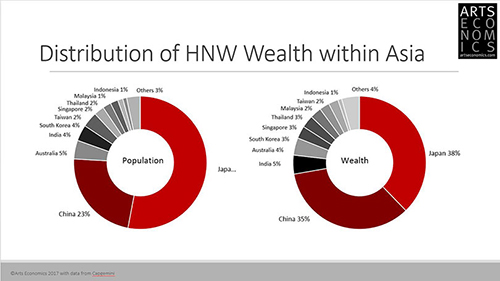

Japan and China are still the largest regions in Asia, in terms of HNW wealth and the population of high net worth individuals, but there are many other smaller countries with relatively high pockets of wealth, and these are generating important art collectors, who are buying locally alongside internationally from markets around the world.

The positive wealth dynamics, in terms of income growth and the relatively small share of those yet engaged in the market, is promising. New middle class consumers in Asia, who are perhaps not yet buying art to any large extent, could create important new customer segments in the art market over the next decade.

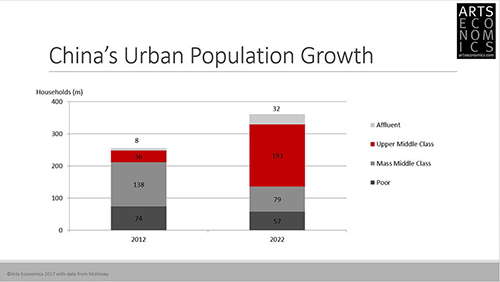

In China, for example, GDP per capita is still less than one quarter of the average in Europe, and less than 15% of the US, and the majority of the Chinese public does not yet have the disposable income to enter the art market. But with average incomes growing at over 300% in the last decade and a burgeoning middle class, the potential for future art sales is very positive. China’s urban population is set to expand by at least 30% in the decade to 2020 and it is within this urban population where the most growth is expected in the middle-classes. The upper-middle-class is expected to grow the fastest, to become the largest segment of the population by 2022. This is a critical development that could bring much more depth to the art market in China.

Money isn’t everything. Having a large pool of wealth is a necessary feature for a large art market but it is not sufficient. Japan and Australia are good examples of markets with very large shares of HNW wealth but relatively small art markets, with the wealthy collectors from these nations often buying in established centers, such as New York and London. The three important elements required to make a global art market are:

1. Wealth.

2. Highly developed cultural infrastructures, experts, institutions and ancillary services to support the art trade.

3. Favorable regulatory environment, both internally and with respect to international cross-border trade.

The markets in Asia (and globally) that can develop all three of these features will be likely to be the key centers of the art market going forward.

Clare McAndrew: The Asian art market has been, for somebody like me, looks very much at the big picture of what’s going on in the global art market, one of the defining trends of the last decade. It has really changed how the market looks and operates, and it has been of huge importance to my research over the last 10 to 15 years. When looking at the market sales over the last 25 years, you will see that there has been astonishing growth. Starting at the lowest point in 1991, to the peak in the art market in 2014, the art market grew about 600%, so it’s been a huge increase in the value of sales. In the last 10 years, especially a lot of the impetus for that growth has been Asia. It has been sales predominantly in China that added a big chunk to that number, but also purchased by Asian buyers in traditional centers as well as in Asia. Asia has been a phenomenal influence on that growth in the last 10 years. I think its market is now more globally diversified. It might be more internally competitive, but has protected the markets from some of its downside risks. I think if you look at how the market recovered from the recession in 1991, it took possibly 15 years for the market to get back to where it was. Whereas if you look at the recession in 2009, it bounced back straight away. A big part of that was that it wasn’t just relying on the US, the UK, and Europe, it had all this Asian buying and sales. At the time when markets were falling apart a little bit from the global financial crisis, China was especially starting this tremendous boom in sales.

ⓒArts Economics 2017

China and Asia depend on how you define it, and I will leave that to someone who is more of an expert. But if you look at the main Asian countries in terms of sales, they count for about a quarter of the sales on the global art market. As Melanie was just saying, China has been amazing to watch because it has come so far from when I started doing this report several years ago for TEFAF. I think in the first one, China was about 5% back in 2006 or 2007. It has literally come from there to being last year, the 3rd largest market, but temporarily in 2011, the largest market in the world as well. I has really changed the face of the global picture. If you look at the pie graph 15 years ago, it wouldn’t really be on the map at all, so it has been a phenomenal growth and really changed the way the market looks.

ⓒArts Economics 2017

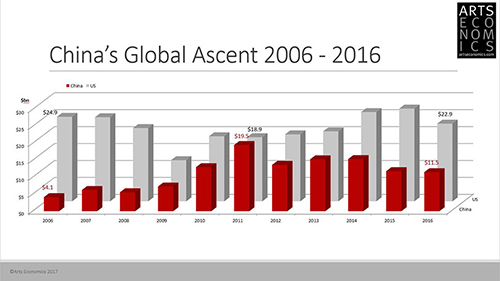

This slide is just comparing two of the major markets at the moment, China and the US, just to show where they came from back in 2006. Even at that stage, the US was more than five times the size of the Chinese market. Then the Chinese market quickly developed, overtook the UK in 2010 and then in 2011 temporarily became the largest market worldwide by a small margin. Since then, sales have been a little bit more subdued, but it is still an integral part of the picture when we talk about the global art market. It’s a very important slice.

Besides sales that happen on the ground, another interesting way to look at the influence of Asia is to look at cross border trades. How much art comes in and out of Asia. This is important as well. China, and especially Hong Kong, have been very important hubs. There are lots of other markets in Asia and I just picked the top five in terms of trade. They are quite local in nature, where a lot of local art is sold. Even for local artists, I think that once they reach a certain level, they then often get sold either in Hong Kong, or in markets even outside of Asia. In terms of exporting, Asia as a whole, has a fairly small share of global exports, whereas the US has a huge share along with the UK. They are entrepreneur markets where things come in and out all the time. The flow of trade is very circular. And again, China is accounting for around half of the exports from Asia. Where Asia has made a bigger dent, I think, is in import as a buyer of art in the world. China is an important part of that, but other markets are important buyers as well. If you look at the top two major auction houses in terms of value, around 30% of their buyers in terms of value now are from Asia. That’s bigger in some cases than European buyers, so it is a huge change compared to 10 or 15 years ago. It’s very much a wealth-driven dynamic to some extent because wealth in Asia has grown and the demand for all luxury goods and art has grown as well. Luxury goods, in terms of wealth economics, have been increasing. That has been met by local sales as well as sales in London, New York and Hong Kong.

ⓒArts Economics 2017

ⓒArts Economics 2017

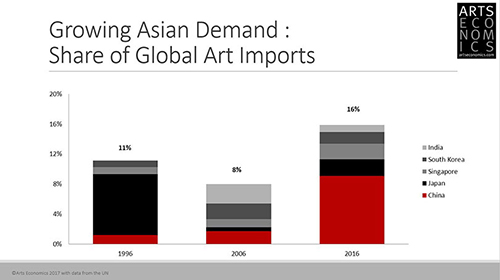

Another thing that’s interesting about imports is who has been doing the buying. If you go back to 1990, Japan counted for 30% of the global imports, which was a huge buyer. This was the famous art bubble that was fuelled by Japanese buying many works in the impressionist sector. It was very much a demand-based bubble. There wasn’t a big inflationary build-up of wealth. Majority of this wealth moved to the property market, however still, there were a lot of buying of the French impressionists’ work; a lot of crazy prices being paid for works that were only of fairly mediocre value. This ended quite abruptly in 1990, when the Bank of Japan raised interest rates. A lot of more speculative people in the market and their wealth portfolios fell apart. Not because of their art collections, but because of their other investments, and the Japanese left the art market. From then on, import buying from Asia was very subdued, and wasn’t really until China came back again around in 2006 that we saw importing start to rise again. We should also mention India, as a big player in the global market at this time in 2006. I remember when I was doing theTEFAF report around that time, there was a lot of speculation about which one, out of China and India, was going to be the big global market to take over. At that stage we really didn’t know which one was going to take off, but it has very much been China, which now accounts for about 9% of imports. The whole of the Asian market is a very important buyer in markets in London and New York.

ⓒArts Economics 2017

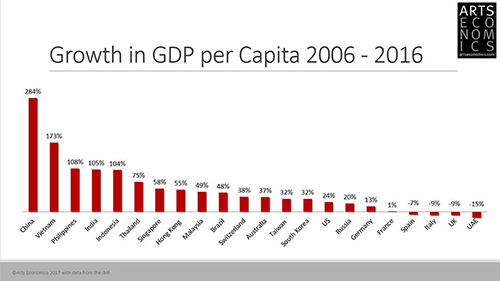

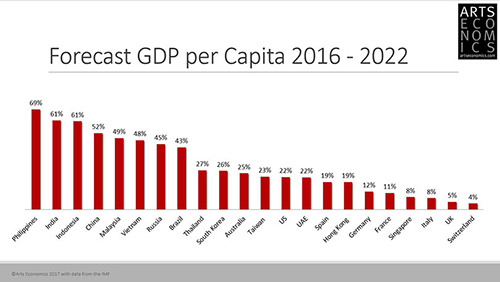

What is driving all this? Wealth is a big factor. This is the growth in GDP per capita over the last 10 years. You can really see that three-digit growth rates are all in that new Chinese economy. Japan is not there, but Japan is quite different because it is very much a mature economy. GDP growth has averaged about 9% over the last 10 years. You will see China, Philippines, India, Indonesia and Hong Kong all growing at rates over 50%, compared to the average of the G7 group about 25%. You will see some very sad statistics for Europe, where incomes are even dropping. It’s a dynamic thing as well, so it hasn’t just happened over the last 10 years. They (China, Philippines, India, Indonesia, Hong Kong) are also forecast to have the fastest growing incomes over the next five years and ongoing. I think it is amazing to think about if you look back in the 1990s, the average income in the US was 70 times the average income in China. If you look at 2006, it was about 20 times. Now, it’s about seven times. So, the gap is really narrowing. Even in countries like China and the other parts of Asia, there is still a small proportion of the population engaged in the art market. We are seeing rapidly growing average incomes and wealth dynamics are very positive signal for potential development in the future.

ⓒArts Economics 2017

ⓒArts Economics 2017

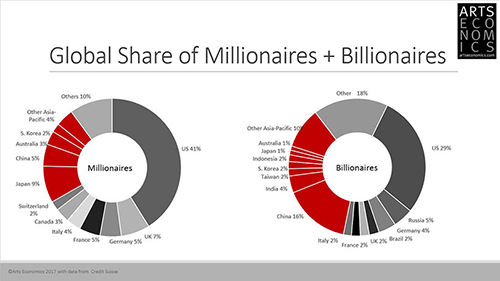

Another really crucial thing for the art market is HNW (High Net Worth) individuals—millionaires and billionaires. What they are spending in the art market is skewed at the top end, so the activities of a relatively small number of people have a big influence on the kind of the research I do on macro figures. This graph shows the population of millionaires and the global share of the millionaire population. The US is still one of the largest homes to millionaires, but the data is flawed when it comes to the definition of some markets. You can see Asia is defined as including Australia and a few other countries. Currently, Asia accounts for nearly 24% of the world’s millionaires and 40% of the world’s billionaires. This is very interesting that the UBS report says a billionaire is created every three days in Asia, which is phenomenal.

ⓒArts Economics 2017

ⓒArts Economics 2017

It is not just the population of Asia, it is also their wealth. This graph displays HNW individuals investable assets over a million dollars and it clearly shows the changing dynamic over time. It was a big thing last year that the wealth in the Asia Pacific region was larger than in North America. From looking at the statistics of HNW individuals from the last 15 years, it was the first time in history it had been that way. It has been very interesting for me to see the way in which it has edged up, that now the Asia Pacific region has more wealth than the US. And this is a forecast. Capgemini and I do the World Wealth Report every year. It is interesting to see that it’s not just about population, but the wealth dynamics. Something big is changing there.

Within Asia, China and Japan are still very much the centers for HNW wealth. In terms of population, Japan is the main country and in terms of wealth, both China and Japan. However, there are other very important countries that are spawning prominent global collectors who, as I said, are not just buying in Asia, but buying out in the world as well, even though their local markets are quite small. It’s not just the influence of the sales on the ground, it’s the influence they are having globally which is important from my perspective. As I said, the dynamics on the wealth side of things is also so positive, because at the moment there is a small fragment of the population. You see millionaires and billionaires in Asia doing a lot of heavy buying, but what countries like China need is an upper-middleclass, which really supports the middle market as well. These graphs are from McKinsey and the projections are very positive. First of all, urban populations in China are growing the fastest and the projections are by 2020 that this upper-middle-class will actually be the largest segment in urban populations. This is the hugely important thing for the art market because it’s very thin in Asia, especially in China at the moment. It’s driven by such small activity, you see such a high buying rate of things in China. Part of that has to do with particular things about auctions and quality, and things like that. Part of it is driven by the fact that there are just not enough buyers, I think, for the suppliers there. This is hugely important dynamic that’s happening.

ⓒArts Economics 2017

ⓒArts Economics 2017

The wealth dynamics are really strong in Asia, but money isn’t the end of it. I don’t think money is everything. Having a large population of HNW individuals is probably a necessary condition for having a good healthy art market, but it’s not a sufficient condition. I always look at Australia and Japan. Those kinds of markets have a huge number of HNW individuals, but they have a really small art market, so there’s more to it.

I was going to say there are three cogs in the wheel. There’s wealth, which we have in Asia, but there has to be something else. The second element, I think, is having a highly developed cultural infrastructure, and this is still developing in parts of Asia and China. We were talking earlier about impressionism and experts and institutions and things like that. These are critical elements. Again, it’s a slightly historical thing, where they are in a phase of catching up with the art market. These things take a long time to develop around the market. Not just the institutions, but the gallery structures and the ancillary services that go with the shipping and all those kinds of things—specialized services that go with the art market. They take time to develop. The last cog, which is a really important one, is the favourable legal environment. That’s both for internally having a market place that encourages businesses to buy and sell art, and also externally. Encouraging a healthy flow of art is also a critical thing. Some countries do it well from one side, for instance they push the art out, but then they don’t let it back in. Other countries are poor on both sides. This is a key element in Asia.

I think if you look at the US, it has really been the key market since the 1950s. The money moved to the US, and the art market followed in a way and stayed there, because it is very well-balanced between having a business-friendly environment that people can conduct business in, they can import and export very easily and it’s easy to do business there. It’s a fiscally friendly environment to do business in. But it’s also a very well protected market place for consumers, where things are guaranteed, to some extent. These are all the factors I think that influence the art market. I think the markets in Asia, once they get all those three elements right, are really going to be the ones that dominate the most in the future.

2. The Diverse Identity of the Asian Art Market ; Adeline Ooi

Adeline Ooi ⓒGallery Weekend Korea

*Draft

Asia and the Asia-Pacific region is a complex region with multiplicitous layers of histories, identities and differing socio-political conditions. This vast continent is divided according to key regions:

◯ Northeast Asia (Japan, Taiwan, Korea): often regarded as the most mature markets in Asia with seasoned collectors, a strong gallery network that is akin to Western gallery models, and well-developed infrastructures

◯ China: exponential economic growth and rapid development have led to dramatic art market growth and dynamic art scene.

◯ South Asia (India, Pakistan, Bangladesh): India was one of the most prominent Asian art markets before the 2008 financial crash. The market recovery is coupled with a strong growing local economy, increasing spending power, and a growing number of collectors.

◯ Southeast Asia (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand, Vietnam): Singapore is the geographical regional ‘hub’. The key emerging markets are Indonesia and the Philippines, which have active local markets and the highest concentration of emerging collectors with sizeable wealth.

◯ Australia & New Zealand: similar to Northeast Asia, with structures similar to the West.

Asia is made up of ex-colonies (heterogeneous societies) as well as homogenous societies (for example Japan, Korea, Thailand) and are often divided by language and belief systems, and differing stages of economic development. As a result, the information flow across Asia is fragmented and does not circulate in a uniform manner (in comparison to Europe or North America).

The Asian art market is impossible to define as one singular entity due to its vast territories. Asia, as an entire region, rarely comes to gather in a single meeting place. In the past, local and regional market activities tend to operate almost exclusively of each other.

Art fairs in Asia have become the platform to bridge these regional markets. Hong Kong and Shanghai have become recent ‘centers’ for art market activities through the presence of 《Art Basel》 in Hong Kong (March), and the 《Westbund》 and 《ART021》 fairs that make up the Shanghai Art Week (November). But is this enough to substantiate an Asian art market?

Given the current conditions of these key regions, it is evident that the respective markets will continue to grow. However, Asia’s multitudinous nature will continue to prevail and the region’s key markets will not flourish uniformly and will continue to evolve in differing stages of development.

Adeline Ooi: Before we go into the future of the Asian market, I think it is very important for us to spend the first 10 minutes talking about where Asia really is because it is a big continent. Usually in my line of work, when someone says to me “I am interested in the Asian art market”, or asks, “How is the Asian art market doing?”, then my first question would be “Which part do you mean?”. I am glad that Clare showed you all of those statistics because in some ways our presentations are very much related to each other. I thought about spending these 10 minutes playing geography teacher a little bit, so just bare with me because I think it’s important to map out the different key regions. Asia is usually broadly defined as stretching from Turkey, all the way across the Pacific, to New Zealand. We know that that’s a lot of landmass to cover and we also know that Asia is at different stages of development. It also has a lot of to do with our history: independence, economic development, a turbulent past, and all the rest of it. Broadly speaking, in art market-speak, Asia is divided into five major regions.

Let’s begin with China, which is probably the most unique case study ever. Thinking about Clare’s statistics over the last 10 years is a colossal jump and everything has grown exponentially. I am sure Chinese collectors are no strangers to all of you because they have headlined the news for so long, whether it’s in the secondary market or the primary market. There has been a lot of talk about young fearless collectors and the proliferation of private museums within the Chinese context.

Next is Southeast Asia, which is probably the youngest region within the Asian context or Asian history. This is a melting pot. As you can see Southeast Asia is made up of about 10 Asian nations, most of which gained independence after World War II. We have had a huge colonial history until recently and I say ‘we’, because I came from Malaysia. I know all too well about the post-colonial hang-ups: the question of identity, history, politics and I’m sure you know about Pol Pot, for example. A lot of this is also the mode of development as you know it.

I think Thailand is actually worth mentioning here because it is a similar case to what happened with India. I remember when I first came back to Southeast Asia in the 1990s. There was so much to talk about Thailand and its artists and great art scene. At that time, the government was doing so much to push Thailand out to the forefront. After 《Venice Biennale》 in 2003, Thailand had a presence in Venice over the next few years until everything went quiet post-Thaksin, post-‘Red and Yellow’ fight for power. It’s a shame because it doesn’t mean that there is no art in Thailand. There is, it’s just that it hasn’t been out for the longest time. At the same time, there were such great artists who should be seen, but have not been brought up for some time.

Then we have Singapore, which is the regional hub by default and in some ways a hub for Asia, Australia, and New Zealand as well. It connects them to Southeast Asia in that sense geographically. Of course, we can’t exclude Indonesia and the Philippines. It was interesting just looking at the chart with the number of billionaires compared to millionaires, where we could see 2% of billionaires in Indonesia compared to no millionaires at all. Indonesia and the Philippines are two of the most prominent emerging markets that we have, which are very dynamic art scenes. Before my job as an art director, I was a curator and specialized in Southeast Asian art, and again, there is a very interesting imbalance there. In Indonesia, there are great collectors who are really passionate about the arts and I mean it in every sense of the word. At the same time, there are wonderful nonprofits in particular cities and very active artists to a certain extent. But at the moment, there are not many active galleries, currently, only two or three major ones. If you compare it to 10 years ago, everyone wanted to open a gallery because it was great business, but again, there has been some imbalance. I think that makes talking about Asia as a whole, quite problematic.

The Indian subcontinent has a story similar to Thailand. In the late 1990s all the way to pre-2008 crash, India was at the forefront. I think we looked at the BRIC countries, and there were definitely wonderful collectors. They were making headlines in terms of growth, but in post-2008, they took such a big hit compared to China. Now we can see it slowly picking up pace again, but still Indian collectors are not that visible anymore in the auctions for example. The local market continues to run and I have heard about so much more activity happening recently. In Mumbai, for example, there are Gallery Weekends going on, and now in Delhi, there is the 《India Art Fair》. Active local scenes are chugging along, but that does not necessarily translate beyond their shows. I think the other thing to also keep in mind is the post-colonial hang-up. India was a strong British colony for a long time, so within the Indian consciousness, I think there is a tendency to look west rather than to look east. For any Indians, the idea of summering in London or New York is common, whereas the thought of them going to Hong Kong is like, ‘Why?’. It has a lot to do with their heritage, history, and their affinity to two different cultures because of how the story of India was shaped.

I forgot one of the most important markets ever: the northeast, which is Taiwan, Japan and Korea. As we know, it’s the most developed and the most mature market in Asia. Seasoned collectors have got a strong gallery network that is perhaps most akin to Western models. It has got great museums. Leeum is probably one of my favourite museums in Asia, where standards are very high and it shows us achievement, aspiration and inspiration.

Having mapped this all out in geographical terms, what I am trying to say is that we are a great mix of ex-colonies, which means that some of our ideas are more heterogeneous than others. There is more racial mix compared to say Japan and Korea, where they tend to be more homogeneous.

The other thing about Asia that we should always bear in mind is that the information flow doesn’t circulate the same way one might expect in Europe or in America. I remember the days when I came back, I was so interested in learning about Indonesia, but there was no information. You have to physically go there and find out and speak to people. Of course the Internet has changed that tremendously. But nevertheless, I think information doesn’t really flow within Asia as one might expect. The notion of Asia as a whole is really difficult to grasp because we are together, but we are not. For example, think about Korea and India. What is the connection there? It might be more common for an Indian to go to Korea now because of K-pop, but in the past there was no connection. It’s a very interesting way of looking at how we’ve grown because despite the Internet and social media, and the fact that the world is happening so much faster now, we are still fragmented in so many different ways. I think there have been more centers. This is why I was going to show you this.

Art fairs, over the past 10 to 15 years, have played a role in trying to bring people together. In the past, there were not many events for Asian art, whether it be biennials, triennials or major art exhibitions. Only since 10 or 15 years ago did art fairs begin to heavily feature Asian works. I remember the early days of 《CIGE(China International Gallery Exposition)》in Beijing or 《SH Contemporary 2007》, that was perhaps one of the first few times we saw so many different galleries from different parts of Asia coming together. I think that was probably the first time I met galleries from India and the rest of Asia. I had a kind of physical interaction with them even if I hadn’t been to their countries. I think the 《Art Basel Hong Kong》 has played a tremendous role in forming a center. We only have five days in a year and I don’t know if that’s really substantial enough to say that we are fully integrated. Now you have Shanghai Art Week, which is coming up in November with splendid 《ART021 Shanghai Contemporary Art Fair》. I think that will be another great gathering of Asians every year. My question is, ‘Is this really enough?’ I want to go back to Clare’s last slide of economic wealth and the other two ‘cogs’ which I can remember right now. Regulations and infrastructure need to be considered because it is an ecosystem. In art markets, we have collectors, galleries, and art market, but the other things we need to consider are the infrastructures. Where are they and are they well-placed? Some countries have a great number of collectors like Indonesia and Philippines, but the other infrastructure is just really not there. There is no government support, there is very little of it and a lot of it comes from private initiatives. It’s a really a big question here. We know that Asia’s market is going to continue to grow because economically speaking, a number of these countries are still growing. They have just begun to flourish economy and publish demographics. It is all great news, but what does it mean as a full continent? I think it is really something that we need to watch and wait.

Gallery Weekend Korea

Organized to support contemporary Korean art's advancement in the international art market, Gallery Weekend Korea is hosted by the Ministry of Culture, Sports, and Tourism and organized by the Korea Arts Management Service(KAMS). It is an international event designed to introduce Korean galleries and artists to leading art professionals and organizations around the world.

-

-

Focus / Features - 26 Dec 2017

Focus / Features - 26 Dec 2017Reviewing Overseas Visual Arts Support in Korea (2) : International Residency Programs in Korea, Current Status and Suggestions